Inflation – A Curated Exhibit

Exhibit A

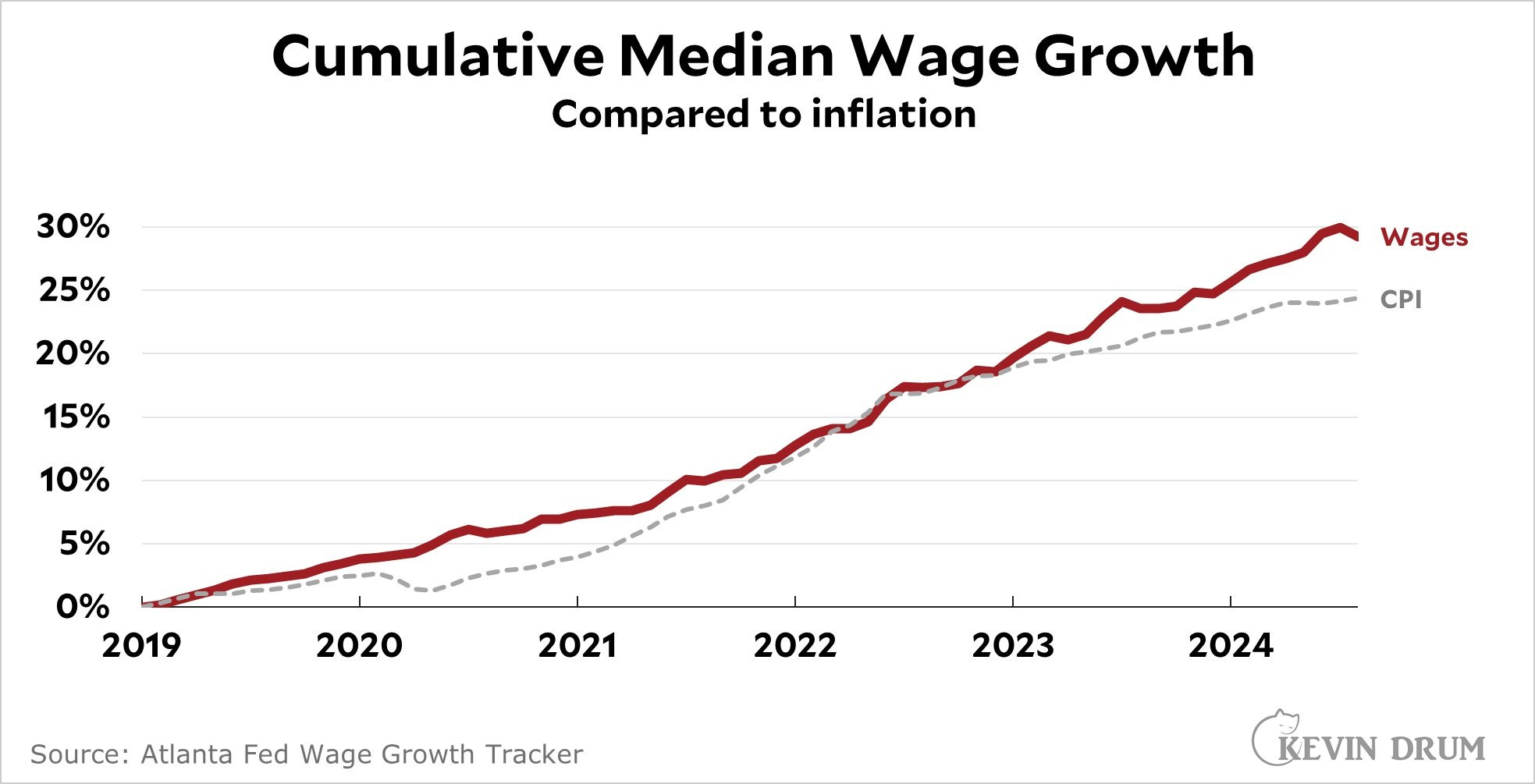

Kevin Drum has produced the single chart that ought to close the book on the story of post-pandemic inflation:

I can only add some emphasis of my own to his tight summary:

After the pandemic, wages outpaced inflation substantially. Inflation later clawed back some of the increase, but wages never fell behind CPI. And thanks to a tight labor market, after 2022 wages quickly started outpacing inflation again. There was never any wage erosion.

Even when inflation was at its peak, real wages were never falling. On the whole (which is the only way aggregate numbers like this work), workers were never worse off.

Why, then, did the mainstream, right- and left-leaning press lose their minds about inflation for an entire 3 to 4 year period?

About a year ago, I spent many hours trying extremely hard to produce a succinct answer to this question. I put together at least 20 drafts of op-eds that I tried over and over again to get someone to publish. But no one wanted to hear it: I failed every time.

Exhibit B

Here’s what I wrote in September 2023:

Inflation is Bad for Rich People

For over 3 years now we have been repeatedly told – from sources left, right, and center – that inflation is bad for poor people. It is not. It is bad for rich people.

All the laments about inflation hurting the poor turn out to be the result of either confused thinking about prices in a capitalist economy, or disingenuous attempts to distract readers from seeing that only the rich should truly fear inflation. We can disperse the inflation fog in a few short steps.

Money is not a commodity, not any sort of “thing” of positive value. Money is a relation between a creditor and a debtor, symbolized by a token (a coin, a bill, numbers in a deposit account), and denominated (named and measured, for example “€50”). The $100 in my bank account is my claim on Citibank; they are my debtor and $100 is what they owe me.

Because money has no value, inflation cannot be understood as a decline in the value of money. There is no inherent value to $100, so there is nothing to decline. Instead, inflation is just the name we give to an overall rise in all prices. Of course, we cannot gather data on the prices of literally everything, so economists create imaginary shopping baskets (which they call indices) of things we need to buy. If the basket cost $100 a year ago, but costs $105 today, then we call that 5% inflation.

Is 5% bad? Is 1% better?

Much of the reporting on inflation simplistically assumes that a bigger number is worse than a smaller one. The basic idea is somewhat intuitive: as consumers we like it when the things we want to buy are cheap, so higher prices must be worse than lower prices. Particularly for people barely making ends meet, it seems incontestable that “higher” prices (for housing, food, transportation, etc.) must be a bad thing. No surprise, stories about inflation come peppered with examples of increased prices of gas, eggs, or daycare – all adding to the daily burden of working people.

But journalists play a shell game with their readers when the pick out examples in this way. Inflation measures the overall price level, the price of everything. Prices of individual commodities go up and down all the time, but the price movement of one commodity is not an illustration of inflation. Inflation cannot “cause” a rise in individual commodity prices because inflation is itself the name for the rise in the price level itself. (Saying the price of eggs is higher because of inflation is like saying a baseball player got more hits because his batting average was higher.)

For example, from June through December 2022 the price of gasoline dropped from $4.92/gallon to $3.21/gallon – a massive decline of 35%. Yet this statistic neither indicates nor proves that the US economy experienced deflation over that time, because gas is just one item in the basket. Significantly, while the increase in gas prices during the first half of 2022 was widely reported, very little was said about the massive drop in prices in the second half of the same year.

The inflation number tells us nothing on its own. The only way to know if inflation is good or bad is to compare it to something else. What we compare to depends on our time frame.

In the short term, we should compare to income, which economists conceptualize as a “money flow” (an amount coming in over a set time period). If price levels go up 5% in a year but my income goes up 8%, I am better off. The meaningful statistic here is not inflation, but “real wages” – a measure of income that accounts for inflation. If real wages are declining, your monthly income buys less; if real wages are growing, it buys more. Looking at real wages from 2019 (pre-pandemic, and pre-inflation) to today, we see that they have risen. Despite inflation, the median wage buys more goods than it did before.

In the long term, our comparator is wealth, which we can visualize as a “money stock.” Crucially, this “stock” of money can either be a money asset (a claim you hold against a debtor in the form of a savings account, a 401k, etc.) or a money liability (a debt you owe to a creditor in the form of a car loan, a mortgage, etc.).

Unlike the short term, where inflation has no absolute effects, in the long term, inflation erodes money stocks.

Say that today I have a salary of $60,000 and I borrow $300,000 (five times my salary) in the form of a mortgage and car loan. Now imagine that over the next ten years annual inflation averages 6% and real wages stay flat, raising my salary to $108,000. In 2033, I will owe significantly less in economic value than I did in 2023. The amount of money I owe will itself purchase significantly less in goods and services, and my income to debt ratio will have shrunk dramatically (from 5/1 to less than 3/1). Armed with this basic knowledge we see one way to solve the student loan crisis: run the economy with higher levels of inflation, thereby dissolving the debt.

Who would this hurt? Answer: the wealthy. Inflation destroys wealth by reducing the purchasing power of a dollar in the future, while low or no inflation preserves wealth. Making inflation into a monster provides a smokescreen, hiding the fact that inflation truly harms the rich (those with financial assets), while it helps those with debt who work for a wage.

The effort to portray inflation as an enemy to us all serves to hide an important conflict among us: that between those who have wealth and those who do not. We can only depict inflation as a dangerous predator, if we also admit it has a very specific prey – namely, rich people. For anyone with accumulated wealth, inflation proves to be a genuine threat. But one person’s wealth is another’s debt, and for the 30% of Americans who have negative net worth, inflation can be a hero.

Exhibit C

After getting the above turned down by everyone I could think of, I woke in November 2023 to read a published op-ed in the Sunday New York Times that urged the Fed to start buying mortgage-backed-securities in order to “save” the housing market. It was written by a guy who sells mortgage bonds – a seemingly relevant fact that the Times failed to note. The self-interested hypocrisy was so plain, the vapidness of the argument so obvious, that I thought, at the least, the NYT might publish my letter to the editor.

That was deeply naive of me: of course they didn’t run my letter. So I’ll run it here:

To the Editor:

Re “The Fed Has Put Our Housing Market in Jeopardy,” by Daniel Alpert:

In recommending that the Fed start buying mortgage-backed securities, Mr. Alpert has confused the health of the US economy with the health of investment banks that sell or hold mortgage-backed securities on their balance sheet.

High interest rates are not making housing less affordable for most people: rents are down year-over-year, with October marking the steepest decline in rents ever measured on a key national index. And unlike 2008, mortgage-backed securities are not toxic assets that the Fed needs to buy in order to ensure the solvency of banks.

Mr. Alpert is right that buying mortgage bonds would allow the Fed to artificially push down mortgage rates. But this will only prop up historically sky-high housing prices, thereby exacerbating the problem of affordable housing.

This might be a good idea for firms – like Mr. Alpert's – that sell mortgage bonds, but it’s a bad idea for the American people.

Exhibits D, E, etc.

If we learn nothing else, the “Inflation Panic” of 2021–2024 should serve as some indication that we lack any sort of firm grasp of the basics of inflation as a real-world set of practices and experiences. I can’t help but blame the intuitive, seductive pull of the orthodox theory of money, and its tempting presentation by Milton Friedman: if money is a commodity with value, then “inflation is always and everywhere a monetary phenomenon.”1

Of course, Friedman has it 180 degrees backwards: inflation is never a monetary phenomenon. This is the case because while money is a measure of value under capitalism, it is not a standard of value. There is no standard of objective value. David Ricardo proved this by devoting his entire life to finding such a standard, and repeatedly reporting his (failed) results: it cannot be found because it does not exist.2 All value/price changes are relative changes. You can literally never know if something goes up/down in value/price; you can only ever know if it goes up/down relative to something else. Inflation cannot be defined as the loss of value of money, not only because money has no value, but also because no single value can change intrinsically; it can only move relative to other values.

An inflation index measures the prices of a basket of goods, but there can be no real meaning given to changes in that index unless and until we compare it with other prices/values. Hence the importance of Kevin Drum’s chart, with which I opened this exhibition. It compares CPI to wages, and shows wages have risen more than the prices of the basket of commodities in the CPI.

I would argue this is probably the single most significant comparison to draw, but we need to see that there are many, many prices/values across the global economy, and the relative movements are almost limitless. Most significantly, as I suggested in my op-ed above, a lot of people don’t really care about median wages relative to CPI; they care about the growth of corporate profits, or the growth in their financial assets. And it is absolutely possible for wages to go up relative to CPI, while profit rates and the return rates to investments in stocks and bonds go down (again, relative to CPI).

If we want to develop a better theory of inflation – or even just a better intuitive grasp on what is going on when price indices move – we need to be looking at the relative movement of various prices/values. To start, I would suggest at least three main comparators.

Relative prices of specific commodities or commodity sectors

Even back when inflation indices were showing low or no inflation, we know that the costs of things like health care, daycare, and education were rising rapidly relative to the prices of most other commodities, and far outstripping growth in wages.3Price indices relative to median wages

This is Drum’s chart, and I would suggest that no story on “inflation” should ever be written that doesn’t provide an updated copy of it. Inflation means nothing on its own.Income generated by a sum of capital (money) at the “riskless” market rate…relative to CPI, to median wages, etc.

In other words, if I buy $1 million in US treasuries, what will my investment be worth at the end of the year, and how will its purchasing power compare to the beginning of the year. Also, if I consider the interest as an income generated by the principal, then how will that annual income (about $50,000 in 2024) compare to median wages?

This is a very rough framework; even so, it can throw matters into stark relief: The real worry in 2022 was not that inflation was outstripping wages (it wasn’t) but that it was outstripping the riskless return rate (it was). And the most direct result of the Fed intervention was to fix this: in 2024 the riskless return rate exceeded inflation amply.

Finally, Chris Stocking has also pointed me in the direction of a number of other excellent “exhibits” – that is, generative ways to start rethinking the phenomenon we call “inflation.”

Here’s The American Prospect’s rich collection of articles on pricing.

And here’s Steve Man’s “Notes Toward a Theory of Inflation.”

Everyone knows this famous quote from Friedman, but perhaps too little attention is given to the lecture from which it is drawn (the quote appears at the end, presented as a summary of his own argument). It comes from an address Friedman gave in India, one targeted to the context of a growing, “developing” economy. The piece rewards patient reading because it develops an odd, unique model that combines Schumpeterian circular flow with Keynesian “demand for money,” along with a deeply orthodox (Mengerian) commodity theory. This all adds up to the conclusion that more money supply must decrease the value of each unit of money. Friedman thus seems to sincerely hold that if a government issues bonds first, inflation will not occur, but if they pay in government notes first, it will. (He thus shares with Stephanie Kelton the curious belief that without bonds there is no government debt.)

We have Piero Sraffa to thank for patiently documenting Ricardo’s lifelong search.

I would suggest that this was portrayed as less of a “universal crisis” (compared to the recent panic over “inflation”) because those high prices were associated with high corporate profits in those sectors.

I loved this article. I was hoping you would address, though, differential purchasing patterns by income bracket. That is, median wages outstripping the CIP only tells us something interesting if increases to the CPI hit all incomes roughly equally. But if much of the rise of prices comes in, e.g. used cars, purchased more frequently by lower income buyers, (not to mention if wages increase faster at the top of the scale than at the bottom) then inflation becomes bad for poor people, too. No?